The coronavirus pandemic, which has caused U.S. GDP and employment to drop at unprecedented rates, left economists and policymakers blind at a moment of enormous strain for millions of workers, businesses, and government officials trying to cope with the crisis. Macroeconomic decisions are usually informed by federal statistics, typically published with a month- or year-long time lag, and are often measured at a national or state level, making it difficult to analyze the economic activity of specific populations in real time

Recognizing the need to rapidly measure the pandemic’s economic shock on a granular level, four economists—Ackman professor of economics Raj Chetty, economics professor Nathaniel Hendren, postdoctoral fellow Michael Stepner, and associate professor of economics John Friedman of Brown—have worked with private companies to build the Opportunity Insights Economic Tracker, a platform that makes anonymous, aggregated private-sector data on consumer spending, employment, and other essential metrics publicly available. “What we wanted to do was to measure and develop a real-time economic tracker that relies on private-sector data, that can make that information available to the policy community and help guide better decisions as we manage this crisis,” Hendren said. What they have found illuminates unusual differences in consumption behavior among low- and higher-income families, and the disproportionate impact of the pandemic-caused recession on the services sector versus the traditional recession impact on goods and manufacturing.

In a paper released today, the researchers used data from the tracker and found that the COVID-induced economic downturn, at least in the first few months, has been fundamentally different from previous recessions. “The health origins have really driven this crisis along very different pathways than [other] recessions in the U.S.,” Friedman said.

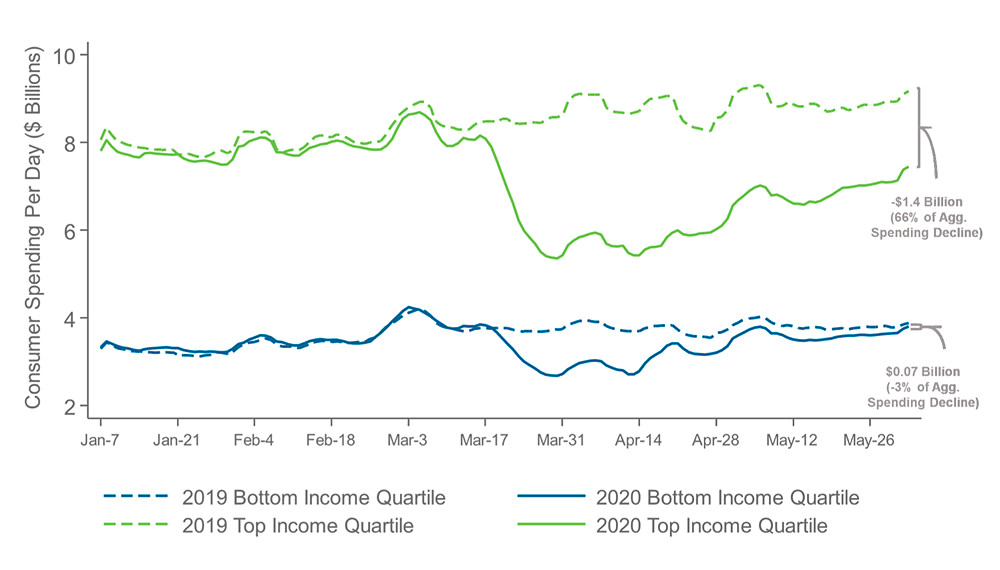

A typical recession hits low-income people living in low-income neighborhoods—who are more vulnerable to layoffs and business closures—hardest. Spending decreases and new unemployment claims tend to be concentrated in those areas. But this has not been the case during the pandemic: through May 10, the wealthiest quartile of households has accounted for more than half the reduction in U.S. consumer spending, while the bottom quartile accounted for 5 percent. This is not because wealthy people are losing money—high earners who can work from home were less likely to have lost their jobs. Instead, the authors believe that as the pandemic spread across the country, the wealthy spent dramatically less on discretionary services at restaurants, salons, and other business because they feared infection. Indeed, neighborhoods with higher rates of COVID infection saw greater reductions in spending. “What we see is that high-income Americans reduce their spending much more than low-income Americans, and they also stay home more,” Stepner explained. “What is clear is that high-income people are either better able to stay at home or are more worried about going outside and interacting with others, so they cut back dramatically on their spending. And in particular the sectors that are hardest hit are the ones that involve in-person, face-to-face interaction”—the places where, of course, many of those lower-income workers make their living.

Consumer Spending Changes During COVID Crisis, by Income Group

In a typical recession, spending on physical goods drops, while spending on services like haircuts hardly changes. But during the pandemic, services have accounted for more than two-thirds of the spending reduction. Spending on luxury goods that don’t require in-person contact, such as pool installations or landscaping, actually increased, which further suggests that fear of contracting or spreading the coronavirus, rather than income loss, is driving spending reductions and revenue falls. “If you thought that…people who would otherwise be putting nice pools in their backyard were fearful about their economic outlook, then you would expect declines in those sectors,” Hendren said. “We don’t see that. We see declines in sectors that really require that in-person contact.”

As the wealthy spent less on in-person services, enjoying the privilege of avoiding going out themselves by relying on deliveries, low-income workers who provide services in affluent neighborhoods bore the brunt of the unemployment burden. Small businesses in affluent neighborhoods suffered a 60 percent revenue loss in the richest 5 percent of ZIP codes in the United States, compared to a 40 percent reduction in the poorest 5 percent of neighborhoods. In some cases, the gap was much greater: small businesses in New York City’s Upper East Side lost 73 percent of revenue, compared to 14 percent in the East Bronx. Small businesses in wealthy neighborhoods were more likely to close, and job postings in those neighborhoods have decreased, which may slow long-term recovery. “Low-income people who work in service-sector jobs that cater to rich people are disproportionately the ones who are suffering in this economic crisis,” Stepner explained.

Yet spending drops among low-income people have been limited so far, due in part to the government stimulus that gave $1,200 to most citizens, as well as to increased unemployment benefits. Low-income household spending rose by 26 percentage points after the stimulus, compared to 9 percentage points for higher-income households—consistent with economic theory that has long suggested lower-income households will spend such money, while wealthier ones can add such funds to savings and were accordingly excluded from most of the stimulus checks (see below for discussion of other elements of the federal recovery and stimulus program). “The stimulus checks were a key component of supporting the disposable incomes of low-income Americans,” Stepner said. “But it’s only going to last so long.” The COVID-induced economic downturn can still turn into a more traditional recession, where high-income families’ spending recovers and low-income people who can’t return to work suffer sustained income losses and decreased consumption. “That’s yet another reason why we think this tracker is really important,” Stepner added: “to provide policymakers and researchers with that real-time picture into how things are evolving across different communities and different people within those communities.”

Although the stimulus payments provided much-needed cash aid to families, the authors argue, they did not actually do much to help the businesses reliant on in-person services that were forced to close by the pandemic—in part because the payments did little to increase spending in those high-income areas where spending reductions were concentrated. Moreover, they found that following the stimulus payments, spending on durable goods rebounded to pre-COVID levels, but spending on in-person services remained less than 50 percent of the baseline. These spending reallocations, which had already started pre-stimulus, could portend more permanent shifts in economic activity, Friedman said. “Even though spending is returning close to normal, spending on things like travel is still really essentially zero,” he added. “And similarly, people are buying a lot more online, they’re buying a lot more durable goods, they’re buying fewer in-person services than before.” Of course, the reason for that is obvious—the pandemic. “The usual argument for stimulus is to try to increase demand to businesses that could then retain their workers,” Hendren explained. “But right now, the limit for why people are not connecting is the virus, not the lack of demand on the part of people who are getting the stimulus.”

The study examined the economic impact of two other government interventions: the Payment Protection Program (PPP)—which provides forgivable loans to small businesses on the condition that all employees are retained at 75 percent of their pay—and state-mandated economic shutdowns and re-openings. The PPP, a program that has cost over $500 billion, did little, the researchers found, to improve unemployment at small businesses: hours worked declined at almost identical rates at businesses that were and weren’t eligible for the program. The authors hypothesize that this is because PPP loans were not targeted at firms at risk of losing employees. Instead, because the loans are forgivable only if a business doesn’t fire anyone, the program incentivized firms already at low risk of employment loss to apply for what was essentially free money. “The firms that signed up may have been precisely those firms that were already planning to keep their workers on,” Stepner said. “And so the firms that didn’t feel that they were able to keep their workers on didn’t sign up and didn’t end up keeping their workers on, and the money potentially went to the firms that are already best able to weather this crisis.”

State-mandated shutdowns and re-openings, too, did little to influence economic activity. Comparing across states that shut down at different times, the authors found people had already begun cutting back their spending due to fear of the virus at roughly the same time, regardless of the timing of official rules. “It’s really a perception of the virus that is driving a lot of the behavior that we see, not the formal dates of when the shutdowns are happening,” Hendren said.

Instead of broad stimulus packages, like checks to all households or loan programs for all small businesses, the authors suggest providing targeted benefits to people who have lost income. “In any program with a fixed budget, there’s some benefit to targeting,” Stepner said. The trillions of dollars that have been spent in only a few months to relieve the pandemic’s economic shock, over the long term, may be unsustainable. Targeting cash aid to those who have lost their jobs, or targeting small-business relief to companies at risk of losing employees, the authors argue, could be more effective. Perhaps those findings will inform a subsequent round of federal stimulus, on which Congress may act in July.

Yet it’s also possible that no combination of economic policies will resolve what is ultimately a health crisis. “If the source of the crisis is that people don't want to go outside their house and buy things because of fear of the disease, in some sense, you’re never really going to get back to normal until you fix that underlying problem,” Friedman said. “And so I think in this case, public-health policy is really a form of economic policy.”