Highlights:

- Endowment valued at $32 billion as of June 30, up $4.4 billion (16 percent) from $27.6 billion a year earlier.

- Harvard Management Company records 21.4 percent investment return on endowment assets during fiscal year 2011.

- All asset categories yield positive returns.

- Harvard’s performance narrowly exceeds its market benchmarks and the principal measure of large endowments’ returns.

- Investment managers caution about impact of recent volatile markets and adverse economic conditions on future returns.

HARVARD’S ENDOWMENT was valued at $32 billion as of June 30, the end of fiscal year 2011—up 16 percent from $27.6 billion at the end of fiscal 2010—according to the annual report released by Harvard Management Company (HMC) on September 22. During the fiscal year just ended, HMC recorded an investment return of 21.4 percent on endowment and related assets—a gain in value of perhaps $5.8 billion to $6 billion, using a back-of-the-envelope calculation. This was a strong performance following the 11.0 percent return in fiscal 2010, and further recovery from the negative 27.3 percent investment return during the financial market upheavals in fiscal 2009, when the endowment’s value declined by the daunting sum of nearly $11 billion. According to Wilshire Associates Trust Universe Comparison Service, large institutional investors achieved a fiscal year 2011 median investment return of 20.1, reflecting the generally favorable market conditions prevailing during the period. Results for the other similarly managed large university endowments (Yale, Princeton, Stanford) have not yet been reported; early figures from Cornell, Penn, and the California pension pools have indicated investment gains for the fiscal year ranging from 17 to 23 percent.

The difference between the rate of investment return and the growth in the absolute value of the endowment reflects the distribution of endowment funds to support University operations and for other purposes (perhaps $1.4 billion in fiscal 2011, down from fiscal 2010’s $1.56 billion, fiscal 2009’s $1.66 billion, and fiscal 2008’s $1.63 billion), offset by endowment gifts received during the year (as an estimate, perhaps in line with the quarter-billion dollars received in fiscal 2010). (Exact investment returns, endowment distributions, and gift figures will be disclosed in the University’s annual financial report, to be published in mid to late October.)

The arithmetic—gross endowment gains, less distributions, plus gifts, equals net endowment growth—is important. HMC’s fiscal 2011 investment return again handily exceeded its long-term goal of 8.25 percent annual gains. After distributions in support of University spending (the endowment now provides about 35 percent of operating revenues), this return, plus gifts, enabled the endowment to grow in absolute terms at about three-quarters the robust rate of the investment return. Given the current low rate of inflation, that 16 percent appreciation in the endowment represents vigorous real growth—and acceleration from fiscal 2010, when the value of the endowment rose 5.4 percent (after accounting for distributions made and gifts received).

Is the endowment all the way back from the white-fingernail performance of fiscal 2009? Hardly: its peak value was $37.2 billion at the end of fiscal 2008 (and $35.4 billion a year earlier). But the strong results for fiscal 2011 surely provide a measure of comfort and relief. As HMC president and chief executive officer Jane L. Mendillo wrote in her report on the most recent results, “The return on the Harvard endowment for the year…was strong.” Citing the investment professionals’ active management of the portfolio to satisfy growth, liquidity, and risk-management objectives, she continued, “We are pleased to report that our progress in fiscal year 2011 was significant along each of these dimensions.”

With fiscal 2011 on the books, HMC’s annualized investment return for the past five years rose to 5.5 percent from 4.7 percent last year, and for 10 years to 9.4 percent from the prior-year 7.0 percent. Part of the improvement, of course, reflects the strong fiscal 2011—and part the arithmetic of moving beyond fiscal 2001 (when investment returns for the endowment as a whole were negative 2.7 percent, in the wake of the dot-com collapse). More significantly, these rates of return look more like the long-term returns that HMC’s investment strategy is designed to produce. And most importantly, it is the long-term performance that shapes the Corporation’s financial decisions as it reviews Harvard’s budget and determines a safe and appropriate rate of distribution from the endowment to support University operations. During the current fiscal year 2012, the Corporation authorized a 4 percent increase in the endowment distribution, following two years of declines. What decision it has made, or will make, for fiscal 2013 is not yet public.

Performance Details

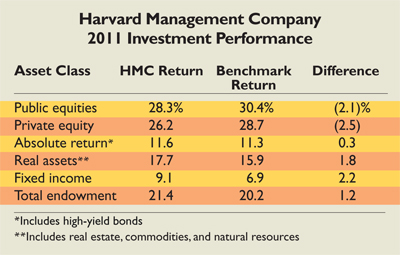

ON A RELATIVE BASIS, HMC's 21.4 percent return (after all investment-management fees and HMC operating expenses) exceeded the 20.2 percent return calculated using market benchmarks for the assets in the “policy portfolio.” (That is what HMC calls its model for allocating assets among categories such as equities, fixed-income instruments, real estate, and so on.) HMC also bested its benchmarks in fiscal 2010 (the 11.0 percent HMC investment return versus 9.4 percent for the policy portfolio)—a welcome recovery from fiscal 2009, when HMC’s performance trailed its market benchmarks by 2.1 percentage points. In both 2010 and 2009, the University’s portfolio—which is highly diversified, and geared toward long-term appreciation—fared less well than the median return of the Trust Universe Comparison Service (a popular measure of large endowment funds), in part reflecting dissimilar asset allocations: TUCS funds are about half invested in public equities (versus one-third for HMC’s policy portfolio), with only a few percent invested in real assets (typically almost one-quarter of HMC’s allocation). Out-performing that metric for fiscal 2011 gives HMC at least public bragging rights.

By asset class, using the categories introduced in its reporting in 2009, HMC’s fiscal 2011 performance (with comparison to each external benchmark) was:

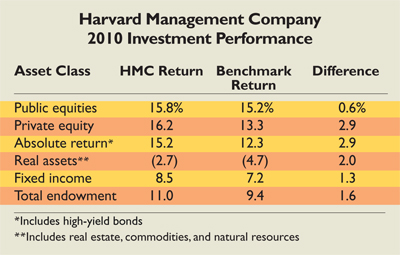

(For comparison purposes, fiscal 2010 results by asset class appear at the end of this article.)

Two overall observations:

- First, market returns were strong across the board during fiscal 2011. As Mendillo put it in her letter, “Many of the sectors in which we invest experienced robust returns during the year ended June 30, and a number of our strategies within those markets did quite well.”

- Second, for HMC, all asset classes produced positive returns—a happy result reflecting gains on real-estate assets, following punishing loses for HMC and other investors in commercial properties following the 2008-2009 financial crises.

In her letter, Mendillo highlighted the performance of certain segments. Investments in domestic equities yielded a 34.6 percent return—comfortably above market indexes. But both developed-market international equities and emerging-market equities trailed their benchmarks, pulling down public-equity performance overall. (Each of these three public-equity classes is assigned an 11 to 12 percent weight in the policy portfolio, summing to about one-third of typical endowment holdings.)

Private-equity investments now account for another 12 percent of the policy portfolio, and produced a 26.2 percent return, also behind the benchmark—but given the frequent lags in reporting private-asset values, it may not make sense to focus too much on the one-year result. Over the long term, HMC has done very well in private-equity investing, but Mendillo last year signaled a more restrained view of this asset class, given both increased competition in the market and the inherent liquidity risks. (She wrote then that “the field of private equity has become more and more crowded—with capital, with managers, and with investors—over the last decade. Our expectations…are that returns will be more muted going forward.” Accordingly, although HMC expects to maintain “a meaningful level of exposure to this asset class over the long term,” those investments will be more concentrated, entrusted to a smaller roster of “our highest conviction [investment] managers.”)

Returns on the “absolute return” category, 16 percent of the policy-portfolio allocation (and consisting of both high-yield fixed-income investments and hedge funds) were 11.6 percent, fractionally above benchmark results. Mendillo’s report does not provide separate figures for performance for the different assets.

Real assets (23 percent of the policy portfolio, consisting of real estate and natural resources, such as timber and agricultural land—each about 9 percent of the endowment assets—plus publicly traded commodities) produced positive returns of 17.7 percent, 1.8 points better than the benchmark, with gains in each segment: 18.8 percent for the natural-resources investments; 11.0 percent for real estate, as noted (a recovery year, but lagging behind the relevant benchmark); and 26.9 percent for the smaller commodities pool.

Fixed-income returns (11 percent of policy-portfolio assets, excluding high-yield bonds, as noted above) were driven by results in the foreign-bond segment (up 21.7 percent), Mendillo wrote. Her report did not categorize returns by domestic, foreign, and inflation-indexed bond investments.

HMC Initiatives

IN CATEGORIZING THE YEAR, Mendillo cited HMC’s confidence “that our portfolio…is well positioned to support Harvard’s mission.” She noted, “The endowment value has not returned to its pre-crisis level. Given the University’s high degree of dependence on the endowment for its operations, we are ever-more convinced that strengthening the portfolio for steady growth over many years will yield the best long-term results for Harvard.” That confidence follows changes in strategy, investments, and coordinated financial management with the administration that, as she wrote last year, “more closely aligned HMC with the University,” following the harrowing months in late 2008 and early 2009 when long-term investments were out of sync with Harvard’s urgent need for liquid resources.

“The much improved flexibility of the portfolio we are managing” that Mendillo cited last year (the result, she said then, of “attend[ing] closely over the last two years to liquidity, capital commitments, and risk management”) shows up in a small, but symbolically significant, tweaking of the policy portfolio. For fiscal 2012, it increases commitments to equities by 2 percentage points (to 48 percent of the assets), but does so with higher goals for public-equity investments and a one-point reduction in private equities. Although there are minor refinements of other targeted asset allocations, the goals for absolute return, real assets, and fixed-income investments remain unchanged.

Meanwhile, the protective policy allocation to cash (2 percent in fiscal years 2009 and 2010, meant as a clear signal to portfolio managers, after HMC had for years boosted returns by borrowing up to 5 percent of its total holdings to invest more, thereby running a cash-negative position) has now been done away with. In the normal course of managing the endowment, the portfolio may occasionally be slightly cash-positive or -negative; but with a more liquid posture overall, HMC apparently no longer feels the need to penalize performance (by holding a formal cash reserve) to buy that sort of insurance against unusual circumstances.

As a sign of the portfolio’s repositioning, uncalled capital commitments—contractual obligations to provide funding in the future to real-estate and private-equity investment managers—have apparently been reduced further, to about $5 billion currently (down from $6.5 billion at the end of fiscal 2010, $8 billion a year earlier, and $11 billion at the end of fiscal 2008). With the endowment again growing and more liquid overall, that level of future obligations to investors in illiquid asset classes (which also include the internally managed natural-resources holdings) that HMC requires to achieve its growth goals, appears to be a comfortable way to proceed, as the asset managers put funds to work in the future in volumes HMC anticipates and desires.

Operationally, Mendillo highlighted some new skills on her staff: an in-house trader of Chinese equities; an in-house commodities-trading team; and a credit-markets group that pursues opportunities in publicly traded corporate debt (HMC has heretofore focused on U.S. Treasury and foreign sovereign debt instruments, not corporate securities).

Consistent with HMC’s direction since Mendillo became president and CEO in mid 2008—just before the financial crisis peaked—HMC continues to bring more of its fund management in-house, citing gains in performance where it can build expert teams (as in the natural-resources portfolio); better control over assets and knowledge of market conditions; and lower operating expenses. From a 70-30 external-internal mix of funds under management when she arrived, the proportion has shifted to perhaps 65-35 today. Continued gradual evolution along that path, at that rate, would not be surprising.

Warnings about the Investment Outlook

If HMC were able to click its collective heels and duplicate fiscal 2011’s performance this year, the endowment would, next June 30, recoup the losses recorded in fiscal 2009. But as Mendillo took unusual pains to point out, the external environment is very unpromising, and the investment markets that behaved so favorably during fiscal 2011 have done anything but since the early summer. As of the release of HMC’s annual report, in fact, amid signs of slower economic growth worldwide, various stock market indexes have declined about 10 to 20 percent just since July 1—a punishing start to the new fiscal year. And lower growth means lessened demand for commercial office space, lower commodity prices, and so on.

Accordingly, early in her message, Mendillo emphasized “the extreme volatility that has gripped financial markets in the months since our fiscal year closed” and noted—specifically in her language about the portfolio’s favorable long-term position relative to Harvard’s needs—that it was “impacted by adverse markets.”

Lest anyone miss the message and assume that all continues well in Harvard’s endowment or the world, she reiterated the warning in her concluding paragraphs: “Since the end of the fiscal year the markets have been exceptionally volatile, driven by concern and uncertainty related to the debt ceiling debate, the fate of the euro zone, the S&P [Standard & Poor’s ratings service] downgrade of the U.S. Treasury securities, and indications of slowing growth in economies at home and abroad.” That litany of worrisome news, she made clear, has tangible consequences: “The impact of these issues on our portfolio is unavoidable.”

So, rather than banking on a continuation of fiscal 2011 investment returns or loosening the spigot on distributions from the endowment, the administration will likely practice, and the extended Harvard community ought to expect, fiscal discipline. All the more reason, eventually, for the endowment-bolstering effects of a substantial University capital campaign.

The University news release appears here.

_______________________