HIGHLIGHTS:

- Endowment valued at $32.7 billion as of June 30, up $2.0 billion (6.5 percent) from $30.7 billion a year earlier.

- Harvard Management Company records 11.3 percent investment return on endowment assets during fiscal year 2013, after negative return in prior year.

- Public-equity assets lead positive returns; positive fixed-income returns despite a down bond market; real assets only category to trail benchmarks.

- Harvard’s overall performance exceeds its market benchmarks by 223 basis points and comes close to returns recently reported by some other institutions.

As the University set about raising a lot of money (launching its $6.5-billion Harvard Campaign on September 21), it was also earning a fair amount: the endowment rose 6.5 percent, to $32.7 billion, as of the end of fiscal year 2013, this past June 30, Harvard Management Company (HMC) reported today. The endowment was valued at $30.7 billion at the end of fiscal 2012. The growth during the year just ended represents the interaction of three factors:

- appreciation. HMC’s in-house and external money managers earned an aggregate 11.3 percent investment return on endowment assets (after all expenses) during fiscal 2013, compared to the -0.05 percent decline during the prior year.

- distributions. The endowment’s value is reduced by distributions to support Harvard’s operating budget, and other distributions for one-time purposes (“decapitalizations”). The operating distributions totaled $1.4 billion in fiscal 2012, and likely increased by 4 percent to 5 percent during the most recent year; decapitalizations, which can vary widely from year to year, were $308 million in fiscal 2012. (Comparable figures for the most recent fiscal year become available with publication of the University’s annual financial report later this autumn.)

- gifts. Finally, the endowment’s value is augmented by capital gifts received during the year. That sum totaled $273 million in fiscal 2012; it will be interesting to see whether the volume rose in the most recent year, during the quiet phase of The Harvard Campaign; as disclosed in the 2012 annual report, early fundraising apparently resulted in strong growth in pledges (20 percent, to $909 million) that year. If the campaign is successful in attracting gifts to endow financial aid and professorships, that should show up in future years.

The endowment remains the largest source of revenue to support the University budget. In fiscal 2012, endowment distributions for operations represented 35 percent of the University’s income—ranging from 85 percent of Radcliffe Institute for Advanced Study revenue down to 14 percent for the Harvard School of Public Health (which is overwhelmingly dependent on sponsored-research funding).

Although the endowment has now recovered somewhat from its post-crisis low of $26.o billion at the end of fiscal 2009, it remains significantly below the record $36.9 billion reported at the end of fiscal 2008—and must support today’s larger physical plant, much-expanded financial aid, and other costs. Those are the considerations the Corporation considers as it sets future distributions (at a time when the level of future federal support for research is especially uncertain, and families’ ability to pay higher tuition bills remains under pressure)—and as it set the $6.5 billion goal for the new capital campaign.

Performance Details

HMC’s 11.3 percent reported rate of return on investments exceeded the 9.1 percent return calculated using market benchmarks for the assets in the “policy portfolio”—the management company’s model for allocating funds among various categories such as stocks, fixed-income instruments, real estate, and so on. (See the 2013 policy portfolio here.) This is the fourth consecutive year in which HMC’s results exceeded the benchmark returns.

The 11.3 percent rate of return is roughly in line with the 11 percent to 12 percent returns for “60/40” allocation portfolios, blending either U.S. or global stock and bond investments in those proportions—a common allocation for many smaller endowments and public pension funds (see comparisons below). Harvard’s portfolio contains a relatively smaller allocation of domestic equities than a domestic 60/40 allocation, penalizing performance in a strong year for American stocks. It has a relatively larger investment in emerging-market equities which trailed U.S. stocks significantly this year, again penalizing HMC versus a less-diversified portfolio. And it maintains a much smaller commitment to fixed-income investments—strongly positive for the endowment in a challenging year for the bond markets (but see below for HMC’s strong performance in this sector).

Characterizing the year, Jane L. Mendillo, HMC president and CEO, said in a news release, “I am very proud of the internal and external managers we have in place and the results they have achieved. Thanks to this talented team, we have made a strong recovery since the global economic downturn of 2008-2009, and our outperformance this year alone contributed about $600 million of additional value to the portfolio over and above the markets.”

University treasurer James F. Rothenberg—a member of the Harvard Corporation, co-chair of The Harvard Campaign, and chair of HMC’s board of directors—said in the release, “The HMC team produced strong results at a time when the revenue streams that have traditionally supported institutions of higher education have been under increasing pressure.” He noted that in addition to exceeding its benchmark for the fourth consecutive year, HMC’s “performance relative to the market was once again positive in most asset categories.”

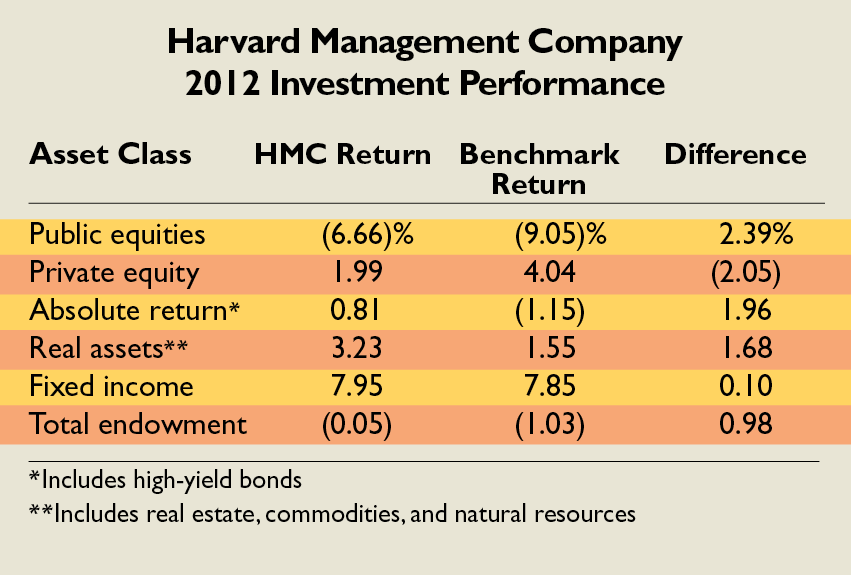

Public equities. After sharply negative returns on international assets in fiscal 2012 (see table below), public stock investments—about one-third of HMC’s assets—rebounded. Domestic equities returned 26.6 percent—5.3 percentage points better than the market benchmark. Developed foreign-market equities returned 20.5 percent—1.6 percentage points ahead of the benchmark. Emerging-market equities recovered from large losses in fiscal 2012, yielding returns of 2.3 percent, slightly less than the 2.9 percent return of the benchmark. Overall, public equities returned 16.3 percent, versus benchmark returns of 14.5 percent.

Private equities. Private-equity and venture-capital investments (about 16 percent of the policy portfolio, up from 13 percent in the prior year) yielded an 11.0 percent return—better than the 10.6 percent benchmark, and much better than the minimal returns in fiscal 2012. But Mendillo characterized this return as only “fair,” given the illiquidity involved in five- to 10-year private investments, which ought to provide some extra return compared to liquid, public-equity stakes. During the past decade or so, that sought-after extra return has not proved out, making it important to hone HMC’s investments in this historically attractive sector with particular care.

Absolute return. These assets (which in HMC’s reporting include both hedge funds and a small portfolio of high-yield, fixed-income instruments, together accounting for about one-sixth of endowment investments) yielded a 13.2 percent return: up sharply from the nominal return in fiscal 2012, and nearly twice the benchmark return.

Real assets. HMC maintains about a quarter of its assets in this category, including natural resources (primarily timber and agricultural land, accounting for half the real assets), real estate, and a small commitment to publicly traded commodities (like oil and natural gas). For the real-assets category as a whole, the investment return was 7.0 percent—the only segment to trail the market benchmark (albeit slightly). Real estate, driven by HMC’s direct investments (as opposed to those made through outside investment managers) again produced strong results, yielding a 10.6 percent return (ahead of the 8.8 percent benchmark return). Natural resources returned 5.1 percent, lagging the benchmark by 2.5 percentage points, an atypical result for HMC in this category. Commodities produced a loss (a return of -4.1 percent, trailing the -3.0 percent benchmark); in the market as a whole, investors did well in petroleum, but poorly in natural gas holdings.

Fixed income. Although HMC does not emphasize bond investments—and has progressively reduced such holdings, while increasing growth-oriented equities of various sorts—its internally managed portfolios often perform strongly. In a year of negative market returns across all segments, HMC’s fixed-income returns overall were a positive 3.3 percent, providing the widest margin of outperformance versus market benchmarks (6.7 percentage points). Domestic, foreign, and inflation-indexed bond returns were all positive for HMC’s portfolio managers.

Other Institutions’ Results

Although it is early in the annual reporting season, among other institutions that have released fiscal 2013 results to date:

- Update September 24, 5:30 p.m. Yale reported a 12.5 percent investment return; after distributions, its endowment was valued at $20.8 billion on June 30. Its peak value was $22.9 billion in 2008.

- The University of Pennsylvania disclosed a 14.4 percent return, raising its endowment value to $7.7 billion.

- The University of Virginia Investment Management Company reported a 13.4 percent return.

- MIT’s investment-management company, MITIMCo, realized an 11.1 percent return, bringing the value of that institution’s endowment to $10.9 billion.

- The enormous California Public Employees’ Retirement System (CalPERS) reported a 12.5 percent return on investments, in line with the 12.7 percent return for Massachusetts state pensions and (according to a Bloomberg report) with the 12.4 percent estimated median return for similar public funds around the nation tracked by Wilshire Associates (the funds that might be most similar to a 60/40 portfolio, discussed above).

Harvard Outlook

For the first time in many years, HMC appears fully staffed. Notable appointments include Jake Xia, chief risk officer, who replaced a staff member who left the organization for personal and family reasons. As reported, Jameela Pedicini became vice president for sustainable investing, a new position. Mendillo’s annual report described HMC as “fully staffed on the investment front with highly experienced, high-quality talent across the board.”

Although HMC has a larger commitment to private-equity and real-estate investments than in the recent past, it appears likely to report capital commitments (obligations to provide future funding to outside managers) in the range of $4 billion to $5 billion: in line with the $4.6 billion shown in the fiscal 2012 University financial report—apparently a comfortable level given the size of the portfolio and the steps Harvard has taken since the financial crisis in late 2008 to assure that it has adequate liquidity at all times.

Characterizing the investment climate—in the week before policymakers in Washington, D.C., determine whether there will be a federal budget, and then whether to raise the national debt limit—Mendillo concluded her report by noting:

The outlook for the world’s economies and markets continues to be full of uncertainty. Questions abound about fiscal and monetary policy here and abroad, about how much “stimulus” is still needed, about the impact of new market regulations and participants, and about the prospects for economic growth across global markets in sometimes shaky political environments.…However, looking beyond some of the shorter-term issues, which we are fortunate to be able to do, we are confident that there is plentiful opportunity for long-term investors like Harvard.

Read the University news release here.